In my post below [an alternative [and disquieting] view…], I was talking about the housing bubble. At the time, I thought I knew what I was talking about, but later, I realized that was an illusion. I was using a term I couldn’t define. Looking around, I decided that that might be because it’s hard for anyone to define the concept. Here’s the Wikipedia definition, as good [and as vague] as any I found:

An economic bubble (sometimes referred to as a speculative bubble, a market bubble, a price bubble, a financial bubble, or a speculative mania) is “trade in high volumes at prices that are considerably at variance from intrinsic values”. While some economists deny that bubbles occur,the cause of bubbles remains a challenge to those who are convinced that asset prices often deviate strongly from intrinsic values. While many explanations have been suggested, it has been recently shown that bubbles appear even without uncertainty, speculation, or bounded rationality. Most recently, it has been suggested that bubbles might ultimately be caused by processes of price coordination, or emerging social norms. Because it is often difficult to observe intrinsic values in real-life markets, bubbles are often identified only in retrospect, when a sudden drop in prices appears. Such a drop is known as a crash or a bubble burst. Both the boom and the bust phases of the bubble are examples of a positive feedback mechanism, in contrast to the negative feedback mechanism that determines the equilibrium price under normal market circumstances. Prices in an economic bubble can fluctuate erratically, and become impossible to predict from supply and demand alone.

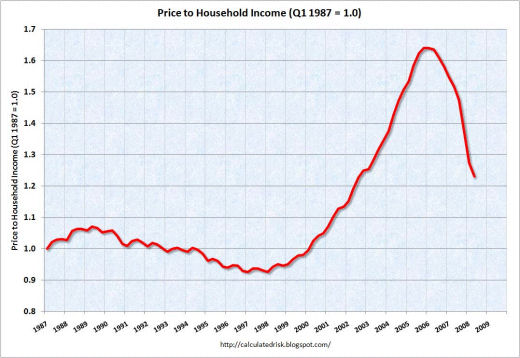

An economic bubble (sometimes referred to as a speculative bubble, a market bubble, a price bubble, a financial bubble, or a speculative mania) is “trade in high volumes at prices that are considerably at variance from intrinsic values”. While some economists deny that bubbles occur,the cause of bubbles remains a challenge to those who are convinced that asset prices often deviate strongly from intrinsic values. While many explanations have been suggested, it has been recently shown that bubbles appear even without uncertainty, speculation, or bounded rationality. Most recently, it has been suggested that bubbles might ultimately be caused by processes of price coordination, or emerging social norms. Because it is often difficult to observe intrinsic values in real-life markets, bubbles are often identified only in retrospect, when a sudden drop in prices appears. Such a drop is known as a crash or a bubble burst. Both the boom and the bust phases of the bubble are examples of a positive feedback mechanism, in contrast to the negative feedback mechanism that determines the equilibrium price under normal market circumstances. Prices in an economic bubble can fluctuate erratically, and become impossible to predict from supply and demand alone.An economic bubble is a situation where some market becomes very inflated [an active market where prices are way above intrinsic value]. The problem is, of course, that one may not know what the "intrinsic value" really is. With the "housing bubble" that’s now deflating all over us, how could we miss it? Here‘s a version of what it looked like:

This is the ratio of the housing price to the buyer’s household income [adjusted to the 1987 value]. Beginning in around 1998-2000, the ratio almost doubled – peaking in 2006. Now it’s headed downward as quickly as it rose.

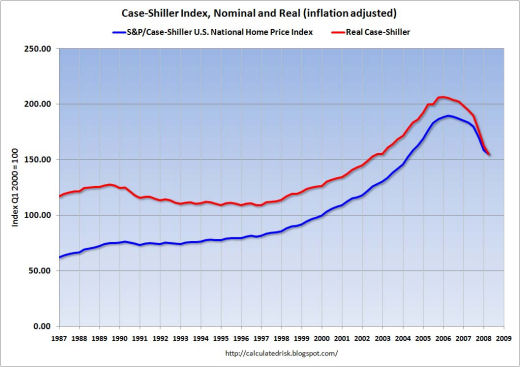

Here‘s another way to look at it, the Case-Shiller Index – the nominal value of residential real estate:

It shows the same thing – a rapid rise beginning in the late 1990’s, peaking in 2006 [more than double], and now on the decline. People were paying an increasingly larger fraction of their income to buy homes [which means that they were taking on an increasingly greater debt load], in the face of the escalating price of housing. Obviously, they were allowed to borrow more based on their income than in the earlier periods. When the house values began to fall, for many, the debt load on their real estate was greater than the new equity value. And many of the creative subprime loans started with lower premiums that rose at some point in the payback period. So with higher premiums on a house that had decreased in [or lost its] value, loan default or foreclosure became a better alternative than trying to either sell the property or continuing to pay on the loan. That threw more property on the market, further reducing prices. Again, from Wikipedia:

Bubbles may be definitively identified only in hindsight, after a market correction, which began for the U.S. housing market in 2005–2006. Former U.S. Federal Reserve Board Chairman Alan Greenspan said "we had a bubble in housing" and also said in the wake of the subprime mortgage and credit crisis in 2007, "I really didn’t get it until very late in 2005 and 2006." The mortgage and credit crisis was caused by a large number of home owners unable to pay the mortgage as their low introductory rate (sub-prime) mortgages reverted to regular interest rates. Freddie Mac CEO Richard Syron concluded, "We had a bubble", and concurred with Yale economist Robert Shiller’s warning that home prices appear overvalued and that the correction could last years with trillions of dollars of home value being lost. Greenspan warned of "large double digit declines" in home values "larger than most people expect." Problems for home owners with good credit surfaced in mid-2007, causing the U.S.’s largest mortgage lender Countrywide Financial to warn that a recovery in the housing sector is not expected to occur at least until 2009 because home prices are falling "almost like never before, with the exception of the Great Depression." The impact of booming home valuations on the U.S. economy since the 2001–2002 recession was an important factor in the recovery because a large component of consumer spending came from the related refinancing boom, which simultaneously allowed people to reduce their monthly mortgage payments with lower interest rates and withdraw equity from their homes as values increased.

What created the "housing bubble?" Did the availability of easier loans allow prices to inflate, or were the loan policies changing to meet the increasing prices? I sure don’t know the answer. I don’t even know if these are the right questions. But what I do know is that the situation has been apparent to for several years, and nothing definitive has been done until  the problem became so great that it afflicted Banks and Mortgage Companies, and later became reflected in the Stock Market.

the problem became so great that it afflicted Banks and Mortgage Companies, and later became reflected in the Stock Market.

the problem became so great that it afflicted Banks and Mortgage Companies, and later became reflected in the Stock Market.

When the blame is partitioned in some future economics textbook, I expect it will have been a "perfect storm" – relaxed regulation, easy credit, "creative loan instruments" with low premiums, greed all around, inept governmental oversight, etc. But like with Hurricane Katrina in New Orleans, once the levy is breached, the clean-up is near impossible. Don’t we wish Mr. Bush and friends had exercised "pre-emption" in this potential economic crisis, instead of in our foreign affairs [the Bush Doctrine]? The "pre-emptive" strike in Iraq has been a disaster. Ignoring the predictable economic crisis here at home for years may have been an even more expensive mistake…

… and my candidate for Director of Obama’s Taskforce on the Economy – Yale’s Robert Shiller – the guy who studies "bubbles." Here’s Shiller on the Bailout…

[…] in the profits coming out of the housing market. As the graphs [also based on Shiller’s data] in my previous post show, the cost of housing relative to income almost doubled during the housing boom – necessitating […]

[…] "bubbleware," virtual money that was not backed up by real value [the virtual economy…, the perfect storm…]. And those retirement plans that have all done so well? I guess that bump in the DOW JONES was […]