Back in the long gone days of Summer 2008, our gas prices were in the $4.00 range. Congress was looking in to the price of oil and why it had risen. A Wall Street Hedge Fund Manager named Michael Masters testified in Congress that it wasn’t because of the obvious – increased demand from China, decreasing world supplies. It was because of speculators. Economists scoffed, including my favorite, Paul Krugman, who refused to accept that escalating oil prices represented a "bubble." Here’s what he said – making fun of the people who believed Masters. He thought they were just looking for a way to blame speculators. By the way, Krugman was wrong. Masters knew what he was talking about:

Congress has always had a soft spot for “experts” who tell members what they want to hear, whether it’s supply-side economists declaring that tax cuts increase revenue or climate-change skeptics insisting that global warming is a myth.

Right now, the welcome mat is out for analysts who claim that out-of-control speculators are responsible for $4-a-gallon gas.

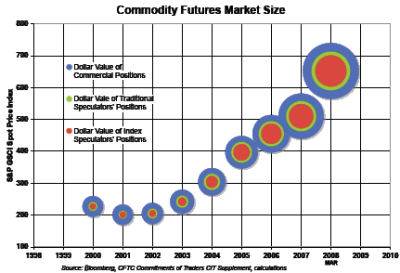

Back in May, Michael Masters, a hedge fund manager, made a big splash when he told a Senate committee that speculation is the main cause of rising prices for oil and other raw materials. He presented charts showing the growth of the oil futures market, in which investors buy and sell promises to deliver oil at a later date, and claimed that “the increase in demand from index speculators” — his term for institutional investors who buy commodity futures — “is almost equal to the increase in demand from China.”

Many economists scoffed: Mr. Masters was making the bizarre claim that betting on a higher price of oil — for that is what it means to buy a futures contract — is equivalent to actually burning the stuff. But members of Congress liked what they heard, and since that testimony much of Capitol Hill has jumped on the blame-the-speculators bandwagon.…In any case, one thing is clear: the hyperventilation over oil-market speculation is distracting us from the real issues. Regulating futures markets more tightly isn’t a bad idea, but it won’t bring back the days of cheap oil. Nothing will. Oil prices will fluctuate in the coming years — I wouldn’t be surprised if they slip for a while as consumers drive less, switch to more fuel-efficient cars, and so on — but the long-term trend is surely up.Most of the adjustment to higher oil prices will take place through private initiative, but the government can help the private sector in a variety of ways, such as helping develop alternative-energy technologies and new methods of conservation and expanding the availability of public transit. But we won’t have even the beginnings of a rational energy policy if we listen to people who assure us that we can just wish high oil prices away.

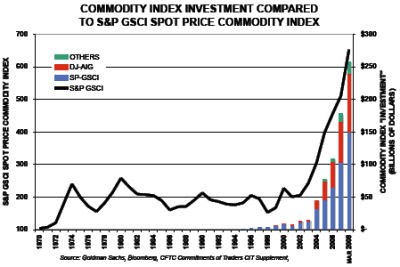

Here are some snippets of what Masters said. It’s a remarkable analysis that predicts with some accuracy the oil bubble crash, and make it infinitely clear why regulation of the Commodity Markets is essential if we are to get out of our financial quagmire. The whole testimony [19 pages] is well worth the read if you have the tolerance for such things. Notice how the spike of index buying parallels the oil bubble:

In the early part of this decade, some institutional investors who suffered as a result of the severe equity bear market of 2000-2002, began to look to the commodity futures market as a potential new “asset class” suitable for institutional investment. While the commodities markets have always had some speculators, never before had major investment institutions seriously considered the commodities futures markets as viable for larger scale investment programs. Commodities looked attractive because they have historically been “uncorrelated,” meaning they trade inversely to fixed income and equity portfolios. Mainline financial industry consultants, who advised large institutions on portfolio allocations, suggested for the first time that investors could “buy and hold” commodities futures, just like investors previously had done with stocks and bonds. Index Speculator Demand Is Driving Prices Higher.

Index Speculator Demand CharacteristicsDemand for futures contracts can only come from two sources: Physical Commodity Consumers and Speculators. Speculators include the Traditional Speculators who have always existed in the market, as well as Index Speculators. Five years ago, Index Speculators were a tiny fraction of the commodities futures markets. Today, in many commodities futures markets, they are the single largest force.15 The huge growth in their demand has gone virtually undetected by classically-trained economists who almost never analyze demand in futures markets. Index Speculator demand is distinctly different from Traditional Speculator demand; it arises purely from portfolio allocation decisions. When an Institutional Investor decides to allocate 2% to commodities futures, for example, they come to the market with a set amount of money. They are not concerned with the price per unit; they will buy as many futures contracts as they need, at whatever price is necessary, until all of their money has been “put to work.” Their insensitivity to price multiplies their impact on commodity markets.

Chart Two shows this dynamic at work. As money pours into the markets, two things happen concurrently: the markets expand and prices rise. One particularly troubling aspect of Index Speculator demand is that it actually increases the more prices increase. This explains the accelerating rate at which commodity futures prices (and actual commodity prices) are increasing. Rising prices attract more Index Speculators, whose tendency is to increase their allocation as prices rise. So their profit-motivated demand for futures is the inverse of what you would expect from price-sensitive consumer behavior. You can see from Chart Two that prices have increased the most dramatically in the first quarter of 2008. We calculate that Index Speculators flooded the markets with $55 billion in just the first 52 trading days of this year.19 That’s an increase in the dollar value of outstanding futures contracts of more than $1 billion per trading day. Doesn’t it seem likely that an increase in demand of this magnitude in the commodities futures markets could go a long way in explaining the extraordinary commodities price increases in the beginning of 2008?

Congress Should Eliminate The Practice Of Index SpeculationI would like to conclude my testimony today by outlining three steps that can be taken to immediately reduce Index Speculation.

Sorry, the comment form is closed at this time.