I’ve included Paul Rosenberg’s summary of this CPI Study as well as a reference to the study itself because the web pyrotechnics on CPI Web Site are a bit hard to negotiate.

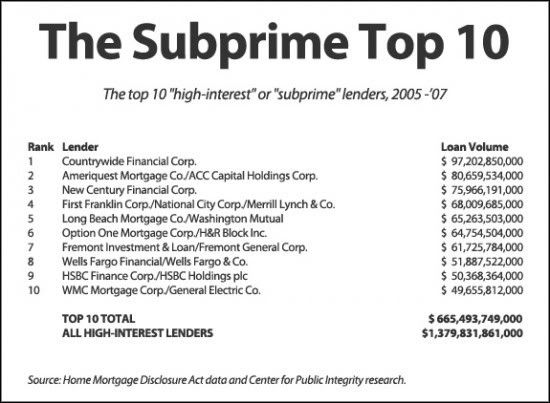

Why would anybody want to make "bad loans?" Since there were well tested ways of predicting who was a poor loan risk, why would anyone see making shaky loans as a way to make money? This Report from the Center for Public Integrity answers that question. Like the biblical character who built his house on sand, it worked out fine for them until it didn’t. I’ve focused most of my attention on the governmental forces that allowed deregulation and the resulting Derivative Market that allowed the process to fester, But that’s a bit like prosecuting the gun manufacturer when someone gets shot. This report is about the people who pulled the trigger.

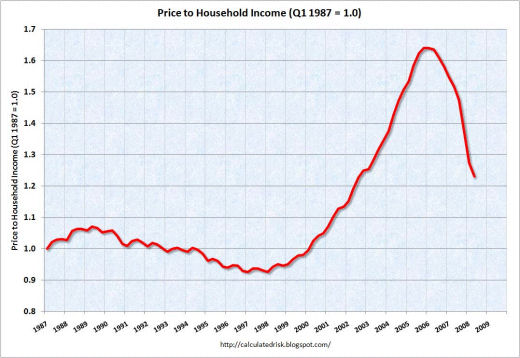

A subprime loan is a loan given to a risky borrower. Those criteria have long been established, mainly based on the credit score derived from previous bill paying behavior. It’s pretty simple, the "best predictor of future behavior is past behavior." The sub-prime lenders emerged saying that no longer mattered. Risky borrowers could now get loans, they just had to pay more for the loan – higher interest rates. But there was even more good news. There’s been a second piece to borrowing – a limit to what you could borrow based on one’s income and assets. The sub-prime loans let qualified people borrow a good deal more than previously [again paying in increased rates]. See the first graph above from the CPI Report. On the face of it, we all assumed that the higher interest rates covered the higher risk of default.

But there was more, a lot more. These Sub-Prime Mortgages were sold ans packaged as Mortgage-Backed Securities. Again, on the surface, it seems like a really swell idea. The Lenders sell their high-yield mortgages for a profit, giving them back their capital for more loans. The buyers get a Security [misnomer?] that pays at a higher rate that anything else. If the package has high-risk loans, if costs less. So, as the graph above shows, the financial institutions suck these things up like hot-cakes. Even better, all this easy money drives up house prices dramatically, and with housing prices are rapidly ascending, if you need to get out, you sell at a profit. Buying and selling houses financed with exotic loans becomes an industry unto itself.

As Tom Jones sang, "What goes up, must come down." In spite of Shiller’s warnings, the housing bubble continued until 2005-2006 when it "burst."

Then, everything that was profitable about the housing bubble became an extreme liability – and the house of cards fell down. A lot of this monopoly money had been "insured" by derivative "credit default swaps" – unregulated and unsecured:

The part that this CPI Report makes abundantly clear is that it is the Sub-Prime Lenders, the ones that cooked up this impossible scheme, the ones that made a killing on the upswing, are the very people we are now bailing out.

There is no issue about whether we need to bring every piece of the machinery that caused this silly scheme to ever exist in the first place under a Federal Watchdog system. We’ve learned that the S.E.C. has been asleep. We’ve seen that there is a sinkhole between the S.E.C. and the C.F.T.C. where the "Derivative Casino" has grown into a cancer that ate our economy. If the Republicans put up a stink about regulating these rogue markets, the only solution is less Republicans.I don’t particularly cotton to a "Free Market" that cuts my retirement investments in half so that these financial raiders can live high on the hog, then require my tax dollars to keep them afloat. You shouldn’t either…

Sorry, the comment form is closed at this time.